The Choosi Financial Red Flags Report 2025

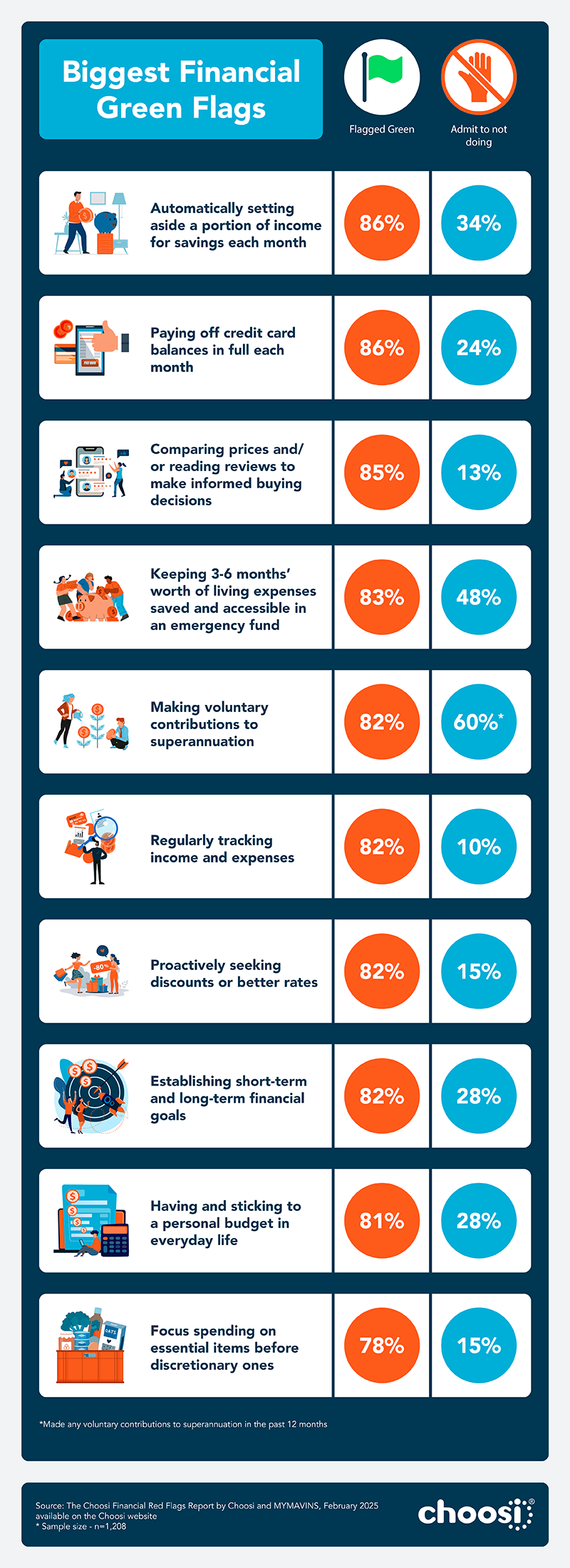

- Majority (82%) of Aussies see setting financial goals as a green flag, yet almost a third don't have any

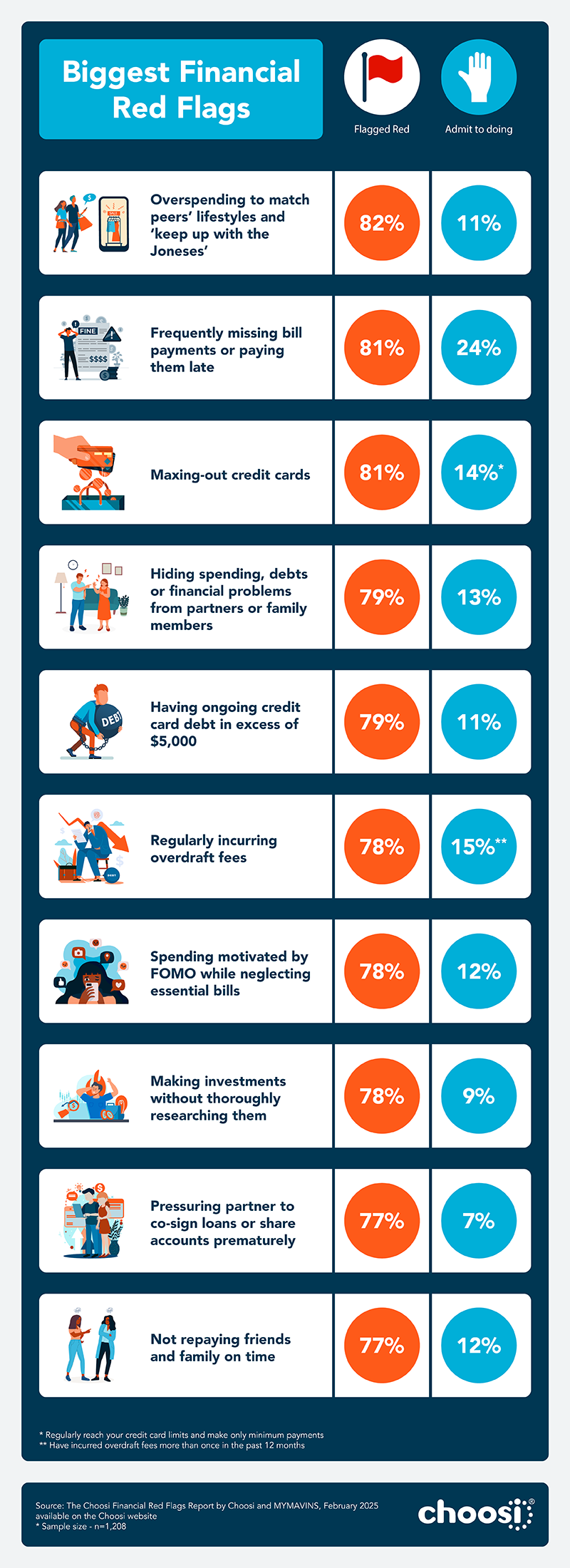

- Almost three quarters (70%) of Aussies consider reusing passwords a red flag, yet 1 in 4 still do it

- Around 2 in 3 Aussies see the absence of car (68%) and home (63%) insurance as red flags, yet at least 1 in 5 remain uninsured

- Nearly 4 in 5 (79%) Aussies view hiding spending, debts, or financial problems from a partner as a red flag

In a world where dating app ‘icks’ and social media ‘red flags’ have become part of our everyday lives, it’s no surprise that this way of thinking has crept into our finances too. Aussies are increasingly looking at money matters through the lens of ‘green flags’ (good signs), ‘red flags’ (warning signs), and those sometimes ambiguous ’beige flags,’ using these signals to judge our own habits and the financial savviness of others.

You’d think knowing what’s good for your finances would mean you’d actually do it, right? Not so fast. The Choosi Financial Red Flags Report 2025 reveals a surprising “say-do” disconnect – for example while the majority of us (82%) recognise setting financial goals as a positive ‘green flag,’ nearly 3 in 10 (28%) admit that we don't actually do it.

As financial pressures continue to plague Aussies, are we all talk and no action when it comes to our finances? Do different age groups have different ideas about what constitutes a financial green, red, or beige flag? And what simple steps can Aussies take to turn financial red flags into green?

Choosi seeks to help Australians make informed financial decisions by simplifying the process of comparing insurance options that suits their needs, budget, and lifestyle. In partnership with MYMAVINS, Choosi wanted to explore the financial habits shaping everyday Australians with The Choosi Financial Red Flags Report 2025. In its latest installment, the study explores how Australians navigate the financial landscape and how they perceive both positive and negative financial behaviours in themselves and others.

Identify your own financial flags and see how you compare

The say-do gap: Knowing vs. doing in financial planning

The green flags, ignored

Setting financial goals is Financial Planning 101, yet it seems many of us have skipped that lesson entirely. While the majority recognise sound financial practices as ‘green flags,’ many fall short of implementing them. For example, while the majority (86%) understand paying off credit card balances monthly is ideal (and a green flag), a quarter (24%) admit to not doing so.

Similarly, 4 in 5 (82%) see contributing extra to superannuation as a smart move (another green flag), yet less than a third (28%) actually follow through, potentially jeopardising their future financial security.

Even having a budget – a fundamental green flag and arguably the cornerstone of responsible financial management – is a financial behaviour that over a third (36%) of Aussies are lacking, raising concerns about the long-term financial well-being of many.

The fear of spending money (FOSM)

FOSM: The new FOMO?

While setting financial goals is crucial for long-term financial health, the report reveals that managing day-to-day expenses is also proving a challenge. As the cost of living continues to bite, Aussies are experiencing a new phenomenon - Fear of Spending Money (FOSM).

The Choosi Financial Red Flags report highlights how more than half (57%) admit to dodging social events due to cost, a trend which is especially strong among Gen X (66%). Interestingly, women are also more likely than men to skip socialising for financial reasons (61% vs. 53%), proving that cost-of-living pressures are hitting our social lives as well as our wallets.

Given the current economic climate, you might expect Gen Z and Gen Y to be budgeting experts. However, surprisingly, they seem less concerned about spending on a night out compared to older Australians. While nearly 9 in 10 Boomers (88%) view skipping bills to go out as a major issue, only 64% of Gen Z and 70% of Gen Y feel the same way.

On the flip side, even though 82% see overspending to 'keep up with the Joneses' as a red flag. Gen Z are four times more likely than Boomers to admit to this (19% vs. 4%). So, while they might be chill about FOMO, Gen Z is still splashing the cash to maintain a certain lifestyle, even if it means stretching their budgets thin.

Risky business: The financial contradiction

Waving both flags

While FOSM reflects a cautious approach to spending, other financial habits revealed in the report highlight that Aussies are taking significant risks despite recognising the dangers. Take investing, for example. While 4 in 5 (78%) of us wave a giant red flag at the thought of investing without research, almost 1 in 10 (9%) admit to doing it anyway.

On the flip side, diligently reading those financial terms and conditions is a solid green flag (68%), but over 3 in 10 (31%) confess to skipping this crucial step. Then there's the beige flag of not having private health insurance. Over half (54%) see it as a beige flag, a "meh" on the financial responsibility scale, while more than a third (35%) still consider it a red flag.

And speaking of red flags, reusing the same password for your financial accounts? Most of us recognise this isn’t 'right' (70%). Yet, despite knowing the risk, 1 in 4 (27%) still do it. So, are we all just a mixed bag of financial flags, waving proudly in the breeze? It seems so.

Couples and money: The cost of love

My money, your money, our secret money

When it comes to money and relationships, the report reveals that things are a little complicated. While most Aussies (79%) wave a massive red flag at the idea of hiding spending, debts, or financial problems from their partner or family, almost a quarter (21%) are unbothered by this financial secrecy, viewing it as a green or beige flag (5% vs. 16%). And even among those who see it as a red flag, close to 1 in 10 (9%) admit to doing it anyway!

Even the seemingly simple act of splitting the bill on a first date can be fraught with financial flags. Over a quarter (27%) of Aussies see requesting a split as a red flag, leading 60% to avoid the conversation on a night out. Interestingly, Gen Z are over twice as likely to ask for a split (29%) compared to Baby Boomers (11%).

And while discussing salary and finances early in a relationship might seem like a green flag to some (38%), it's a red flag for others (25%), leaving many (28%) who want to have the conversation but choose to stay quiet.

For women, the expectation of always paying is a particularly strong red flag (78% compared to 60% of men). With over half (57%) of Aussies already avoiding social activities due to cost (and 62% of Gen Z feeling the pinch), it seems the cost of living might be impacting our dating lives more than we thought.

Tips for the everyday Aussie

As financial pressures continue and the cost of living only seems to be getting higher and higher, financial adviser and co-founder of Fox and Hare Wealth, Glen Hare shares his financial tips for the everyday Aussie.

Bucket your cash flow

Calculate precisely how much of your pay you need for essential bills, dedicated savings goals, and everyday spending. On payday, automate transfers to move your salary into these bank accounts. This strategy removes the temptation to overspend from your main account, effectively automating away bad spending habits. For an extra layer of self-control, consider making your savings accounts harder to access, perhaps requiring a few days for transfers to process or maybe even needing to go into the branch.

Detox your social media feed

Unfollow influencers and social media pages that consistently use their platform to advertise to you. This ambient pressure to buy things can make you feel inadequate about your lifestyle and financial situation when you don’t or can’t. These accounts are designed to encourage spending, not to support your financial well-being. Reclaim your feed, your peace of mind and your money.

Have a "financial date night"

If you're coupled up, set aside dedicated time with your partner to discuss your financial goals for the next 12 months. I do this with my partner every year and it has been transformative for us. We sit down and discuss what we want to achieve, how much we will need to save or budget to make it happen and any adjustments we will need to make. Having a shared ‘why’ behind our savings goals make them so much easier to stick to and it never hurts to have an accountability buddy.

Audit your subscriptions

Take an hour to review your bank account charges and list all your recurring subscriptions. You will probably be surprised to find at least one forgotten service or app that is quietly draining your bank account. Cancel any that you no longer actively use, need, or value.

Meal prep

Most people are disgusted to hear that I prep two meals every Sunday - then eat first for lunch and second for dinner every day, Monday to Friday – but I will not be shamed. The avocado toast scares of the 2010’s were ridiculous and nobody, especially not me, is saying that you can save a home deposit by cutting out avocado toast. Buying lunch and coffee out at work every day is another story completely. Even if it’s not going to buy you a house, $15, 5x per week for 52 weeks is enough for a week in Thailand, Bali or Japan.

Ditch "Buy Now, Pay Later" for everyday items

While credit has its place, using "Buy Now, Pay Later" schemes for everyday purchases or luxury items can quickly drop you into financial hot water. These services make it easy to overspend on things you can't truly afford, creating a cycle of debt. If you can't buy it now, reconsider if you genuinely need it, or save up until you can afford it outright. Of course, credit can be a useful buffer in times of hardship or emergency but do not get caught in the trap of racking up debts buying more than you need or can afford.

Unsubscribe from branded (sales) emails

Your inbox, like your social media feed, is a marketer’s dream and minefield for your financial goals. Marketers send sales and promotional newsletters with one primary aim: to get you to spend money. If you’re trying to save or get on top of your finances, do you really need to make it harder with a self-imposed, daily gauntlet of spending triggers? Triggers that are more often than not customised to hit you right in the spend spot. Just like with the influencers - unsubscribe to reclaim your peace, time, and money. Less temptation in your inbox can very easily translate into more money in your bank account.

Set a daily budget to pay down debt, save or invest

Challenge yourself to reach your savings or financial goals by setting a daily spending limit. At the end of each day, review your expenses. Whatever money is left over from your daily budget, immediately transfer it towards paying down debt, into your dedicated savings bucket or into your investment account. This is an active, fast paced challenge with a nice fast dopamine loop. It’ll keep you engaged and accelerate your progress.

Glen Hare

Glen Hare is a Co-founder and Financial Adviser at Fox & Hare Financial Advice, helping Australia’s 20-45 year olds take buying property, getting invested and achieving financial freedom from a dream, to a plan to a reality. He was voted Australia’s Best Financial Adviser at the 2024 Australian Wealth Management Awards, IFA’s Thought Leader of the Year and has featured on Financial Standard’s Power50 most influential advisers every year since entering the profession. Glen holds a Bachelor of Commerce from Sydney’s Macquarie University and spent his first decade in Financial Services as a banker at Australia’s largest investment bank, Macquarie.

30 Jun 2025