The tax benefits of having income protection insurance

Tax time isn't always everyone's favourite season — but it can be a good opportunity to make your finances work a little harder for you. As you sort through receipts and deductions, one area worth a closer look at is your income protection insurance premiums.

If you've ever wondered, "Is income protection insurance tax deductible?" or "Can I claim it on my tax return?", you're not alone. The good news is that in many cases, it is and you can.

To help us unpack this topic, we spoke with Michael McGowan, Financial Adviser and Founder of Brisbane-based advice firm, Canvas Wealth. In this guide, we’ll break down how income protection insurance can not only support your financial wellbeing but also potentially reduce your tax bill.

Is income protection insurance tax deductible?

This is one of the most common questions around income protection insurance — and for good reason. The short answer? Yes, in many cases, income protection insurance could be tax deductible — it really depends on how your policy is set up.

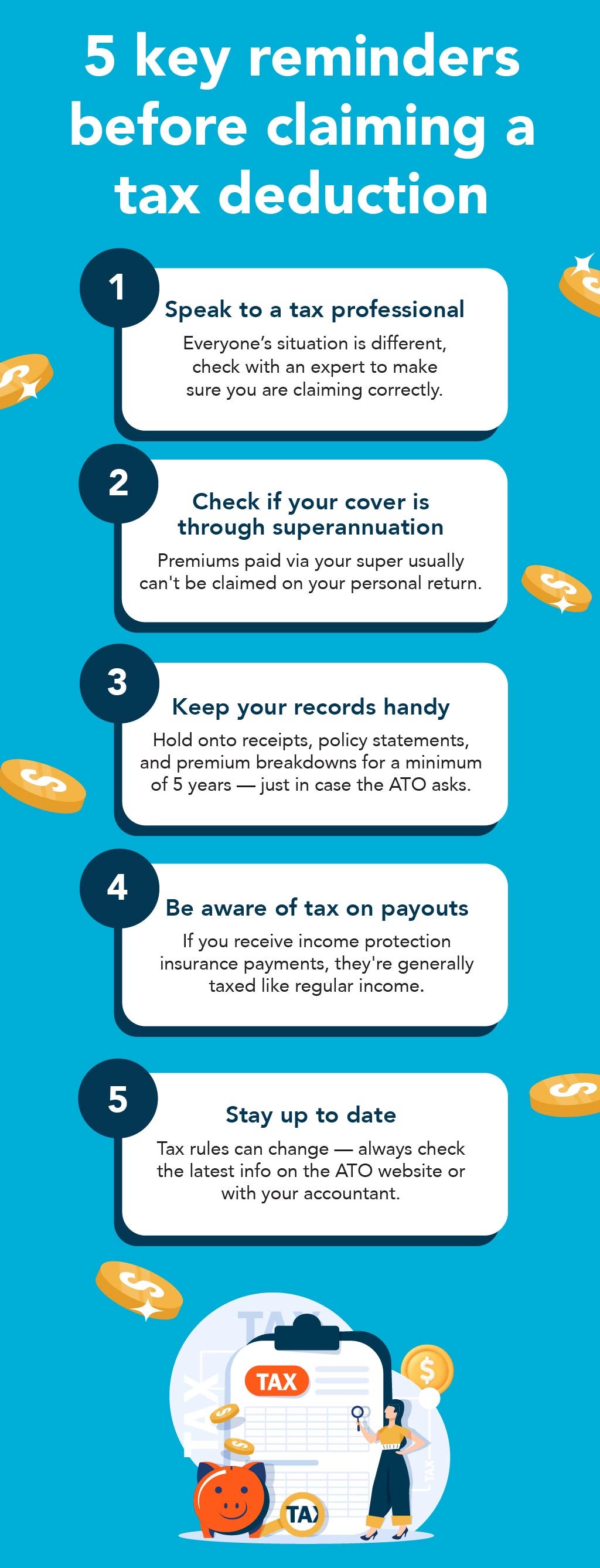

According to the ATO, if you're paying for an income protection insurance policy by yourself (meaning outside of your superannuation premiums), and it's designed purely to replace your income if you can't work due to sickness or injury, then the premiums may be tax deductible. That's because the ATO sees it as a cost directly related to earning your income — just like you would claim for tools or work-related equipment.

"Income protection (IP) insurance helps replace part of your income if you can't work because you're sick or injured," says Michael. "One of the big tax benefits is that, when you pay for income protection insurance yourself (not through super), the premiums are tax-deductible. That means you can get some of that money back at tax time." - Michael McGowan, Financial Adviser and Founder of Canvas Wealth.

Michael offers a helpful example: “Let’s say you earn $150,000 a year and your IP premiums are $3,500. Because you're in a higher tax bracket (paying around 39%), you could get back around $1,365 as a tax refund.”

How to claim your income protection insurance premiums as a tax deduction

It's one thing to know your income protection insurance premium might be tax deductible — it's another to know how to claim it. The good news is the process is generally straightforward, as long as you follow a few key steps and keep the correct records. Here's what you need to know before you hit the submit button on your tax return.

Step 1: Check your eligibility

To claim a deduction, your policy must be held outside of your superannuation and be designed to replace your income if you can’t work due to sickness or injury. This usually includes policies called income protection insurance, sickness insurance or personal accident insurance. If your policy pays a lump sum or is bundled with other covers — like total and permanent disability (TPD) or trauma insurance — it may not be eligible.

Step 2: Keep your records

Hold onto anything that shows what you paid for your income protection insurance — including receipts, bank statements or a copy of your policy. “Your insurer sends you a tax statement each year,” says Michael, “and you (or your accountant) just include it in your return.” You’ll need this information to support your claim if the ATO asks for proof later on.

Step 3: Fill out the correct section in your tax return

When you’re doing your tax return (yourself or through a tax agent), look for the section called "other deductions." This is where income protection insurance claims usually go.

Step 4: Enter the total you paid in premiums

Add up the full amount you paid during the financial year. Make sure it matches what’s in your records — your policy statement or receipts should show this clearly.

Step 5: Double-check your numbers

Mistakes on your tax return can lead to penalties, so make sure your details are accurate. If you’re unsure, a tax adviser or accountant can help.

Step 6: Hold on to your records

Keep your documents for at least five years, just in case you need to show them to the ATO in the future.

Something important to take note of is if your income protection insurance is held within your superannuation, premiums are typically paid from your super balance — not from your own pocket. In this case, you generally can't claim a tax deduction for those premiums.

As Michael explains, “You don’t get the tax refund personally, but the premium comes out of your super balance — so it’s easier on your monthly budget.”

What portion of your income protection insurance premiums can be claimed as a tax deduction?

In many cases, if you're paying for income protection insurance on your own (not through your super), you can claim the full premium as a tax deduction. But there are a few situations where the amount you claim might be reduced — so it's always worth checking the fine print.

Bundled policies

If you've taken out a standalone income protection insurance policy — and it's paid from your own pocket rather than through your superannuation — you'll usually be able to claim the full premium.

However, if your policy is bundled with other types of cover, like life insurance or trauma protection, only the portion that relates to income protection is typically claimable. That's because the ATO only allows for deductions for cover that replaces your regular income if you can't work. Don't worry: your insurer can usually give you a breakdown of how your premium is split.

Policy inclusions

Some policies include bonus features that sound great — like a lump sum payment for serious illness — but these may affect your claim. That's because lump sum benefits don't count as regular income replacement, and only the income protection portion of your premium is tax deductible.

Timing matters

Only premiums you've actually paid during the financial year can be claimed. So, if you pre-pay your policy or catch up on missed payments later, just make sure you're only claiming for what falls in the right year.

Individual circumstances

Michael explains, “Tax law applies differently depending on whether you're salaried, contracting, or running your own business — so it’s always best to double-check."

Are the benefit payments you receive from income protection insurance taxable?

This often catches people off guard. But yes, if your policy pays you a monthly benefit while you're unable to work, that income usually needs to be declared on your tax return. You'll be taxed on it just like any other income.

But if your policy pays a lump sum — for something like serious illness or permanent disability — the rules might be different. Some of these payments may not be taxed, but the trade-off is that premiums for lump sum cover usually can't be claimed as a deduction. So, there's a balance between upfront tax saving and how benefits are treated down the line.

Exploring the benefits of claiming a tax deduction for income protection insurance premiums

For many Australians, income protection insurance offers vital support during difficult times. And the potential to claim your premiums at tax time just adds another reason to keep your policy in place.

Here's how those tax-time savings could work in your favour:

- Helps with cash flow: A smaller tax bill means a bit more breathing room in your budget — whether it’s covering everyday expenses or building up your savings.

- Encourages financial stability: Tax deductions make income protection insurance premiums more affordable, so it's easier to keep your cover and stay financially secure if you can't work.

- Frees up funds for other priorities: Any savings you make at tax time could go towards your superannuation, extra insurance, or simply boosting your emergency savings fund.

- Supports different income types: Whether you’re on a salary, freelancing, or working casual shifts, a tax deduction can help take the pressure off during tax time.

- Encourages regular policy check-ins: Michael adds, “Many Australians don’t have IP cover — and if something unexpected happens, they have to rely on savings, Centrelink, or family. That’s often not enough.” Life changes — from buying a home to starting a family — are a great reminder to check whether your cover still fits your needs.

Why income protection insurance is worth considering

At its core, income protection insurance is about looking after your future — and the people who rely on you. Life doesn’t always go to plan, and if sickness or injury puts you out of work, having cover in place can help you stay on top of everyday expenses like mortgage repayments, groceries, and bills. That kind of peace of mind can make all the difference during a tough time.

And if your policy may also offer a tax deduction? That’s a win-win. Claiming your premiums can lower your taxable income and reduce your out-of-pocket costs — making the idea of cover feel more accessible. Whether you’re getting cover for the first time or reassessing an old policy, tax time is a great moment to consider how income protection insurance can fit into your financial picture.

Keep Reading: Learn about the differences between workers' compensation and income protection insurance.

Because at the end of the day, income protection insurance is about safeguarding one of your most valuable assets: your ability to earn an income. And if it helps you save at tax time, too, all the better.

Not sure where to begin? Choosi can help you compare a range of income protection insurance policies side by side and find cover that fits your needs. Request a quote online today and take a step towards greater peace of mind.

Michael McGowan

Michael McGowan is a Brisbane-based financial adviser and the founder of Canvas Wealth, a financial planning firm dedicated to helping Australians build financial freedom. With a practical and client-first approach, he supports individuals at every life stage — from young professionals to those planning retirement — across areas like insurance, investments, superannuation and wealth management.

12 Jun 2025